ISLAMABAD: The National Electric Power Regulatory Authority (Nepra) announced the new Thar coal tariff on July 27, 2017. It will be valid for two years or until the production of 5,000 megawatts, whichever occurs earlier.

The earlier tariff remained applicable for 2,640MW comprising Engro Power (660MW – two units of 330MW each), Thal Nova (330MW), Thar Energy (330MW) and Thar coal block-I (1,320MW). We keep hearing about the first two projects and not much about the latter two.

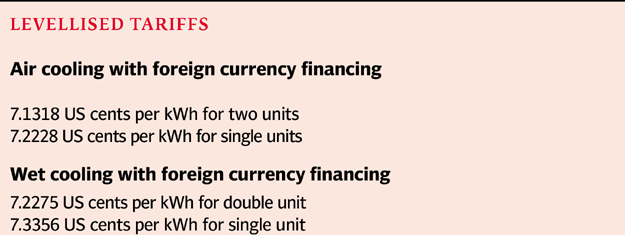

The new thing is that Nepra has introduced two tariff systems – one based on wet (water) cooling and the other on dry (air) cooling. Normally, wet cooling is used and all coal power plants are based on water cooling.

Another imported coal-based plant in Punjab

Most of us are sceptical about the dry technology on account of its lower efficiency, higher capital expenditure (Capex) and higher operating expenditure (Opex). I was also among the sceptics.

However, data provided by the Chinese (Shanghai Electric), who have the right experience, shows something different. They have argued that, in fact, there is not such a formidable difference in case of dry cooling so as to be totally excluded from consideration.

This, in fact, was proved in results of the tariff determination released by Nepra. There is a 2% difference in efficiency and a difference of 0.11 cent in the cost of generation. This is a good news for Thar coal as it was being thought that there would be an upper limit on electricity production from this source. The resource is large, but water availability is a major constraint.

SOURCE: TCEB

The upper limit was calculated by some experts at 10,000MW. Now, with the air cooling technology and it not being uneconomic as well, one could look forward to much higher production levels.

It is a separate matter that due to worldwide opposition to coal and some of the local policies, Thar coal production and financing may be discouraged.

Rate of return

A major issue in the Thar coal tariff was the allowed internal rate of return (IRR) of 20% on equity which translated into 35.4% return on equity (ROE) in operational years. Nepra has reduced the IRR to 18% and has dropped the term ROE, which had created a lot of confusion.

The Sindh government kept insisting on an IRR of 20% thinking that it would be good for Thar coal. But many, including this writer, thought that the opposite was true. The argument of the latter group is that Thar coal has to compete with other sources of energy, even within Sindh, including wind and solar energy. There has been a tremendous drop in international and regional prices of wind and solar power, which have reached 4 to 5 cents.

Nepra has rightly decided on competitive bidding, which will help resolve the controversy spread by vested interests in favour of higher tariff. The 20% IRR was really high, but it was justified for the risk of first few projects and when local interest rates were high at 14%, giving a margin of 6%.

Interest rates today are around 6% and with addition of 6% margin, the IRR comes out to be 12%. Zorlu has submitted a tariff application for a solar power project based on 12% IRR.

Political considerations

Investments are driven by political considerations. Some investors of the western countries will not be attracted by even 20% as proved already in most of the power projects including Thar. Chinese would have considered 12-14% as good enough and would have been attracted.

The energy sector’s success and challenges

There is not much market to sell coal power plants any way. It is a mistake to award an IRR of 18% under pressure from the Sindh government, which has not given much thought to the issues explained above.

The real beneficiaries and vested interests that appear to be behind the higher IRR are local parties. But they will see, it would hurt them and hurt us all.

Another good thing introduced by Nepra in the new Thar power tariff is the reduction in interest rate margin from 4.5% in the case of Sinosure fee application to 4% in case where the company’s insurance rates are not applicable. This was long overdue.

When hard times come to pay in future, one may make a case for downward reduction in other cases retrospectively. It was, in fact, unreasonable to charge a heavy Sinosure insurance of 7% on debt and charge normal commercial rates as well.

Under the non-competitive bidding cases as most of the Chinese CPEC projects are, there is a case of negotiated lower rates of financing under government-to-government arrangements. The logic being that there is higher Capex in such situations. Let us be honest, the upfront tariffs are not that independent. In India, lignite coal tariff is Rs6.6, which in levellised terms may still be lower.

The higher Thar energy tariff is also due to apparently higher coal prices dictated by Thar Coal Energy Board (TCEB). I suppose they are still using the 20% IRR. There has not been any public hearing. The board does not believe in public consultations and prefers working out rates within itself.

Is provincial autonomy such a bad thing so as to preclude transparency and public consultation and oversight? Some reform is required in this respect? If unilateralism prevails, then tomorrow, K-P may ask for an exclusive role in pricing its electricity.

In the first year, the Thar coal cost/price, as expressed in Nepra determination, is $14.75 per ton variable with an unduly high fixed component of $56.43 to give a total of $71.18 per ton.

In later years, the variable component goes down to $10.64 per ton and fixed cost to $19.41 per ton to give a total of $30.05. Accordingly, the levellised cost is $46.50 per ton.

Engro keeps saying that once optimum production level is reached at its mine, the production cost will come down. On the other hand, one keeps hearing of new coalmine investments, all of them submitting similar cost schedules.

If all such new proposals keep coming and are approved, how will that purported optimum level be reached.

Under similar conditions in central Europe, lignite is being sold at $20 per tonne or even lower. In the US, it is as low as $10 per tonne. In India, it is INR 1,500 ($24) per ton.

Reportedly, international consultants had been hired by the TCEB based on which such pricing policy has been prepared. One wouldn’t mind some good royalty payments going to the Sindh government, which it would hopefully spend on the social sector, especially in Thar.

One should look into the possibility of some kind of competition among coal mining companies in order to bring down the cost.

Why are Thar coal prices so high as compared to elsewhere? Firstly, regulated tariffs are almost always high. If competitive bidding is adopted, it is hoped that the prices would come down.

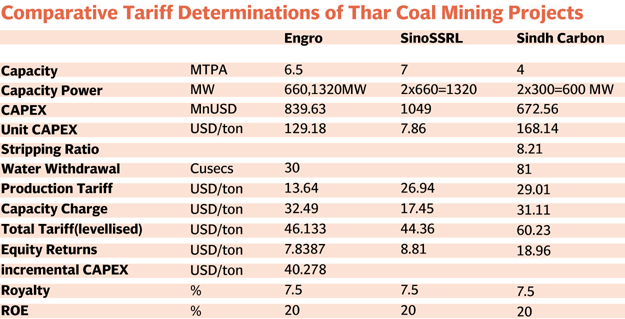

We have provided a comparative table of the three coal tariffs that have been issued by TCEB from which it can be easily seen the rising cost trend, while the opposite ought to have been the case.

What is the logic of entertaining other coal tariff applications, when optimum levels of existing tariff commitments have not been achieved yet, as indicated by Engro figures?

Tying up, coal mining projects with power appears to be the reason, which should have been delinked by now. Old technology such as shovel and trucks might also be the reason for higher costs. One cannot move millions of tons with shovels and trucks. It takes more time and energy. In India and Europe, where most of the lignite mining is being done, bucket wheel excavators have been used. Admittedly, these are expensive and heavy on upfront cash, the unit product cost is lower than that in the case of shovels and trucks.

In Engro’s tariff determination, $161 million of diesel consumption has been shown as Capex.

The cash flow-based tariff calculation model as applicable to electricity tariff has been applied to coal/lignite mining as well. It is unprecedented and not found almost anywhere in the world.

Not only that, very high cost of coal production has resulted due to this and even more importantly, lignite costs as high as $71.18 per ton in the first year results, pushing the first year tariff very high and making it almost unaffordable.

Oil and gas model

Let us take the oil and gas model applied in this country. Does any oil or gas producer require the buyer to pay for his debt repayment and ROE. There is an oil or gas pricing formula according to which the buyer is supposed to pay.

The same applies to coal. It depends on the oil/gas/coal producer to finance his Capex and Opex as he deems fit. The integrated model of Engro being the first project is being pushed too far. This is causing fragmentation preventing economies of scale.

Power generation has to be separated from coal production. Let there be coal mining companies producing and selling coal to the IPPs. There would be operational and transparency issues when the integrated companies would be selling coal to other IPPs.

‘Sindh can make the entire country self-sufficient in energy’

One of the solutions could be to establish Sindh Coal ala Coal India or Gujarat Mineral Development Corporation. Sindh Coal may invite coal mining companies to develop coal mines, independent of the IPPs, buy coal from coal mining companies and sell coal at a composite price or may designate an IPP to buy coal, as is being done in the case of gas.

In a typical mining contract, following is usually done. A minimum off-take is guaranteed, some advance payment is made, there is some pricing formula or a price agreed to with an escalation clause providing for inflation.

This avoids unduly high payment/cash liabilities as are being incurred in the current system adopted by TCEB/NEPRA.

A competitive bidding can be easily organised along these lines. Chinese government may also be requested to cooperate and support such bidding among its own companies, after all its image is also at stake during all this. All stakeholders would benefit if the submissions are considered.

The writer has been Member Energy Planning Commission until recently

Published in The Express Tribune, August 7th, 2017.